English

News Center

—— NEWS CENTER ——

On April 24,2026,the State Taxation Administration issued the positive and negative invoice lists,requiring that “contracts,logistics,funds,and invoices” must be consistent across all four flows。The tax authorities are effectively preventing the “invoice-issuing economy” and supporting the building of a unified national market。

Since April,the national tax system has launched a centralized special inspection campaign targeting the renewable resources industry,and tax bureaus in many places have intensively publicized tax penalties and major tax-related illegal and dishonest cases。Based on publicly released inspection cases from many regions across the country in May—June,typical illegal circumstances and investigation results are reviewed in a centralized manner,sounding a compliance alarm for the industry。

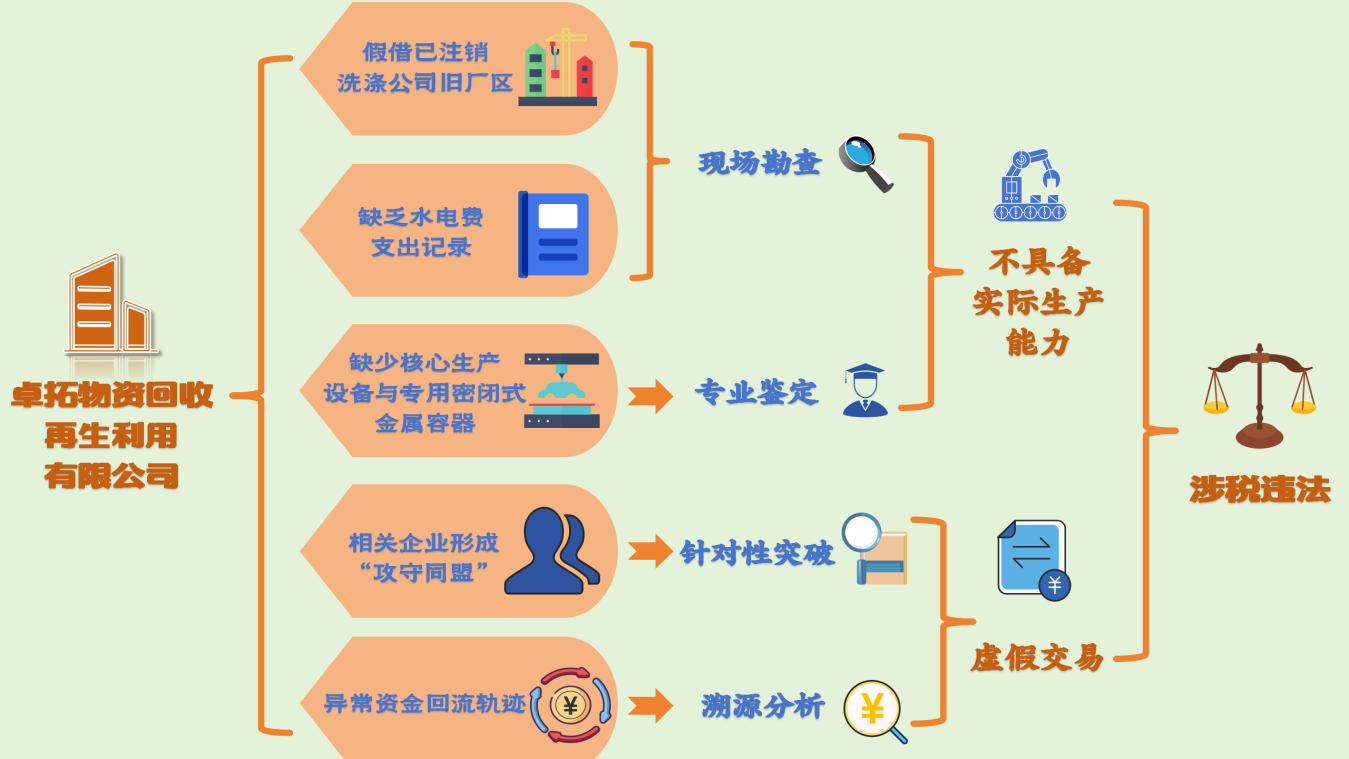

Recently,the Third Inspection Bureau of the Yulin Municipal Taxation Bureau of the State Taxation Administration,based on clues forwarded by relevant departments,investigated and dealt with,in accordance with the law,a case involving 陕西省卓拓物资回收再生利用有限公司 falsely issuing VAT invoices。Upon investigation,from 2020 to 2023,陕西省卓拓物资回收再生利用有限公司,without genuine transactions,had others falsely issue VAT invoices for itself,and then falsely issued VAT invoices to downstream enterprises by charging “invoice issuance fees”。At the same time,the company underpaid VAT and other taxes and fees totaling 324.84 ten thousand yuan through false declarations。In January 2025,the Third Inspection Bureau of the Yulin Municipal Taxation Bureau of the State Taxation Administration,in accordance with relevant laws and regulations,determined that the 183 special VAT invoices issued by 陕西省卓拓物资回收再生利用有限公司,as well as the 214 special VAT invoices and 10 ordinary VAT invoices obtained by it,were falsely issued,and made a handling and penalty decision against the company for tax evasion,requiring the recovery of taxes and fees and imposing fines totaling 641.03 ten thousand yuan,with late payment surcharges imposed in accordance with the law。At present,clues suspected of constituting the crime of falsely issuing invoices have been transferred to the public security authorities for further investigation。Meanwhile,the tax authorities have,in accordance with the law,carried out investigation and verification or opened cases for inspection against 6 upstream invoice-issuing enterprises and 10 downstream invoice-receiving enterprises。

The leftover sign-in register and the vanished water and electricity expenses

Earlier,the Third Inspection Bureau of the Yulin Municipal Taxation Bureau of the State Taxation Administration received clues forwarded by higher-level tax authorities,indicating that 陕西省卓拓物资回收再生利用有限公司 was suspected of falsely issuing VAT invoices。

Preliminary verification showed that the company was registered as an enterprise producing and selling biodiesel,with complete licenses,and chemical instruments and equipment containers were also stored in the factory area,making it appear compliant on the surface。However,a copy of the “Anjie Washing Company Sign-in Register” left at the site attracted the attention of the inspectors。Relying on tax big data analysis,the inspectors found that the production site had originally been the factory building of a washing company。After contacting the person in charge of the former washing company to come to the site for identification,it was confirmed that most of the existing equipment in the factory building consisted of old devices previously used for washing hotel linens。

In response to the inspectors’ doubts,the person in charge of 卓拓公司 argued that the old equipment in the factory building had been modified,and that measuring instruments,delivery pumps,and other equipment specifically used for biodiesel production and processing had been added。When the inspectors further analyzed its tax-related data,they found that 卓拓公司,as a production entity,had no records of any water or electricity expense payments,a phenomenon that clearly violated common business sense。

To accurately assess its production capacity,the inspectors visited universities many times and consulted experts in relevant fields on the process requirements,key equipment,and technical parameters for biodiesel production。After an on-site survey,the experts pointed out that the equipment in the factory building was rudimentary,lacking both core production equipment and dedicated sealed metal containers required for storing finished products,and that it completely failed to meet the basic conditions for biodiesel production。

The above multiple abnormal clues pointed to 卓拓公司 being suspected of falsely issuing VAT invoices。

Fund flows broke the “offensive and defensive alliance”

As the investigation deepened,the inspectors extended the verification scope to the upstream and downstream enterprises of 卓拓公司,but the related enterprises had formed an “offensive and defensive alliance”,with highly consistent statements and watertight answers to key questions such as production and operation,procurement,and sales。One of the companies even proactively provided seemingly complete purchase and sales contracts and logistics records,attempting to disguise fictitious business as genuine transactions。

The inspectors then adjusted their strategy and lawfully obtained the bank account fund flow records of 卓拓公司,finding that shortly after 卓拓公司 issued invoices to downstream enterprises each time,multiple sums of funds were circulated through several personal accounts and eventually flowed back to the payer’s account。This abnormal fund backflow trajectory further corroborated the fact of fictitious transactions。

After integrating multiple pieces of evidence including on-site surveys,professional appraisals,and fund flow records,the inspectors once again conducted targeted inquiries with the upstream and downstream enterprises of 卓拓公司。Faced with a tightly interlocking chain of evidence,the relevant enterprises involved in the case could no longer justify their statements,and admitted the illegal fact that there were no genuine business dealings with 卓拓公司 and that they had jointly participated in the false issuance of invoices。

The disguised scam was exposed,and severe legal punishment was unavoidable

At this point,a false-invoicing chain that used the old factory area of a deregistered washing company and disguised itself as a “biodiesel production enterprise” was uncovered。

Upon investigation,in order to fabricate the procurement costs required for producing biodiesel,卓拓公司,through its network of relationships,had others falsely issue 224 VAT invoices to itself under the names of purchasing corn,industrial oil,catering waste oil,and other items,including 214 special VAT invoices and 10 ordinary VAT invoices,involving a total amount of 2833.22 ten thousand yuan。At the same time,for the purpose of charging “invoice issuance fees”,and in the absence of genuine transactions,it falsely issued 183 special VAT invoices to 10 downstream enterprises,involving an amount of 1796.64 ten thousand yuan。

Paragraph 2 of Article 21 of the Measures of the People’s Republic of China for the Administration of Invoices provides:No entity or individual may commit any of the following acts of falsely issuing invoices:(1)issuing invoices for others or for oneself that are inconsistent with the actual business operations;(2)having others issue invoices for oneself that are inconsistent with the actual business operations;(3)introducing others to issue invoices that are inconsistent with the actual business operations。

In response to its illegal facts,in January 2025,the Third Inspection Bureau of the Yulin Municipal Taxation Bureau of the State Taxation Administration,in accordance with the Law of the People’s Republic of China on the Administration of Tax Collection,the Measures of the People’s Republic of China for the Administration of Invoices,and other relevant laws and regulations,determined that the 183 special VAT invoices issued by the company,as well as the 214 special VAT invoices and 10 ordinary VAT invoices obtained by it,were falsely issued,and made a handling and penalty decision against the company for tax evasion,requiring the recovery of taxes and fees and imposing fines totaling 641.03 ten thousand yuan,with late payment surcharges imposed in accordance with the law。At present,clues suspected of constituting the crime of falsely issuing invoices have been transferred to the public security authorities for further investigation。Meanwhile,the tax authorities have,in accordance with the law,carried out investigation and verification or opened cases for inspection against 6 upstream invoice-issuing enterprises and 10 downstream invoice-receiving enterprises。

Original report link:Fake factory building,old equipment,“real” invoices?——Uncovering 陕西省卓拓物资回收再生利用有限公司_State Taxation Administration

About RESOLAR

Shanghai RESOLAR Energy Technology Co., Ltd. is committed to becoming a recycled material photovoltaic group with deep decarbonization. RESOLAR focuses on technological innovation and builds a world-leading solution for component recycling, impurity removal of damaged cells, recycled silicon materials and cells, and cascaded utilization of components. With professional technology and services, we help customers realize the recycling and reuse of waste photovoltaic resources, and make positive contributions to the development of environmental protection and new energy industries. For more detailed information, you can browse the official website: www.resolartech.com .

Latest developments/news

Contact information

Service Hotline: 13585742918 (Monday to Friday 9:00-18:00)

Enterprise email: ps@resolartech.com (Reply within 48 hours after receiving the email consultation!)

Company Address: Building 8, No. 1528, Wangxu East Road, Fengjing Town, Jinshan District, Shanghai (Caohejing Fengjing Park)